{kind=link}

Why this matters to your wallet

Household cash flow is tighter than it used to be—many people I met in Mexico City after 2020 tightened spending and started hunting for predictable tools. For everyday riders and gig workers, pairing short-term credit with flexible repayment can free up cash for essentials. That’s where a simple move—connecting didi prestamos to the credit features within DiDi Finanzas—can change the math on your monthly budget by smoothing out peaks and troughs in expenses. This isn’t magic: it’s basic credit management and understanding interest rate mechanics so payments don’t spike unexpectedly.

How linking products actually stretches your monthly budget

When you link a small loan product to a flexible credit line, you get two things: predictability and breathing room. A short loan with a clear loan term reduces surprise costs, while an available credit line covers gaps without pushing you into high-cost emergency borrowing. Keeping an eye on APR and monitoring your credit score helps you choose the cheapest path. Over a month, the difference between a well-timed, low-APR draw and multiple micro-borrows can add up to real savings.

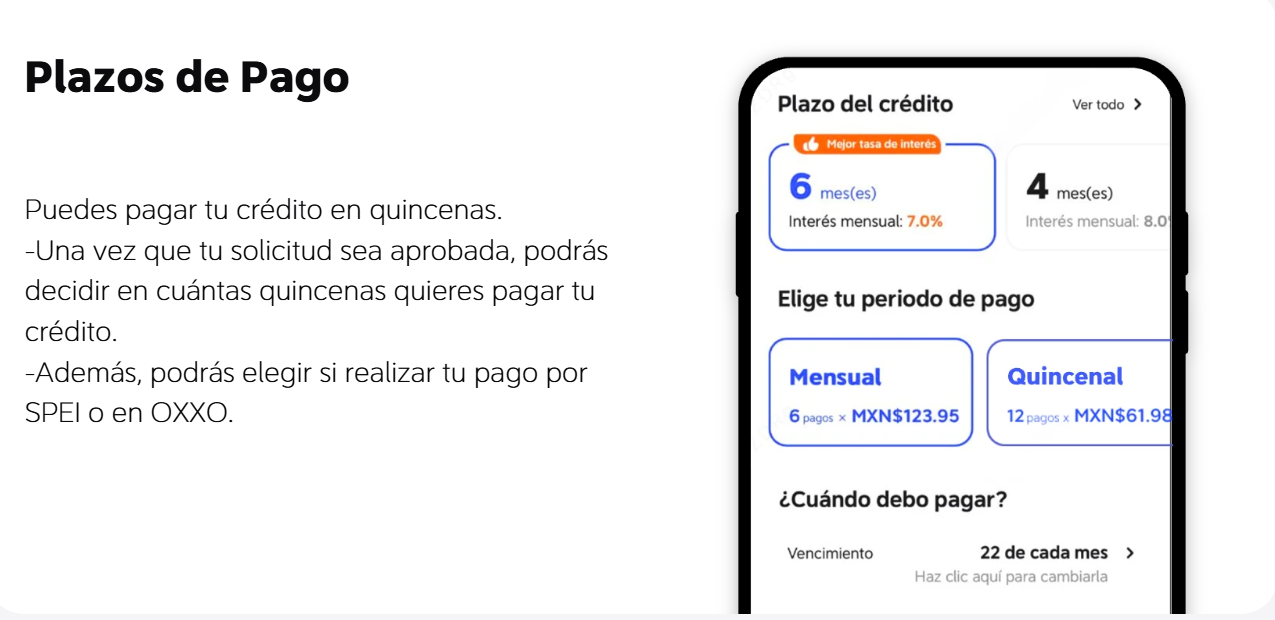

Practical setup: a user-first checklist

Start simple. Follow these steps to make the link work for you:

– Confirm your account identity and link both products in the DiDi Finanzas dashboard.

– Set a monthly repayment plan aligned with pay dates, so automatic payments fall after your main income deposit.

– Use the credit line only for planned shortfalls; reserve loans for one-off purchases with clear repayment timelines.

These moves minimize missed payments and keep fees low. Digital wallets and online lending dashboards make tracking easier, so use them to see balances and upcoming payments in one place.

Common mistakes users make—and the better move

People often treat credit as extra income and keep drawing until interest becomes the problem. That’s risky. Another common slip: not checking the effective APR when comparing offers—labels can hide fees. A better approach is simple: cap monthly draws, prioritize paying higher-interest debt first, and monitor your account activity weekly—small habit, big payoff. Also, avoid simultaneous multiple short-term loans; juggling them raises the chance of missed payments and credit damage.

Alternatives and where DiDi Finanzas fits

Traditional banks, local credit unions, and standalone fintech apps all offer credit. Banks often give lower interest but slower approval; fintechs are fast but can cost more if terms aren’t clear. DiDi Finanzas sits between: it adds convenience for riders and service partners who already use the platform, and it bundles features to reduce friction—payment scheduling, simple dashboards, and in-app notifications. For those who value speed plus decent cost control, that combination is compelling.

Real-world anchor: a quick snapshot

After the initial pandemic shock, many urban commuters shifted budgets to essentials like transport and groceries. Verified reports from major markets showed rising demand for short-term credit to smooth monthly expenses. That trend is exactly why a linked approach—one that combines planned loans with an accessible credit line—became useful for so many people in cities like Mexico City and beyond.

Three golden rules to evaluate your options

1) Total cost over convenience: compare APR plus fees across offers, and model a realistic repayment timeline. True cost guides choices.

2) Flexibility vs. commitment: measure how much buffer you need. If your income swings, prioritize flexible repayment options with predictable fee caps.

3) Visibility and control: choose services that show upcoming payments, available credit, and transaction history in one view—this reduces surprises and lowers missed-payment risk.

These metrics cut through marketing and help you pick a path that fits your cash flow—practical, not theoretical.

DiDi Finanzas brings those elements together in a simple app environment—fast access, clear terms, and tools to keep your monthly budget steady. —